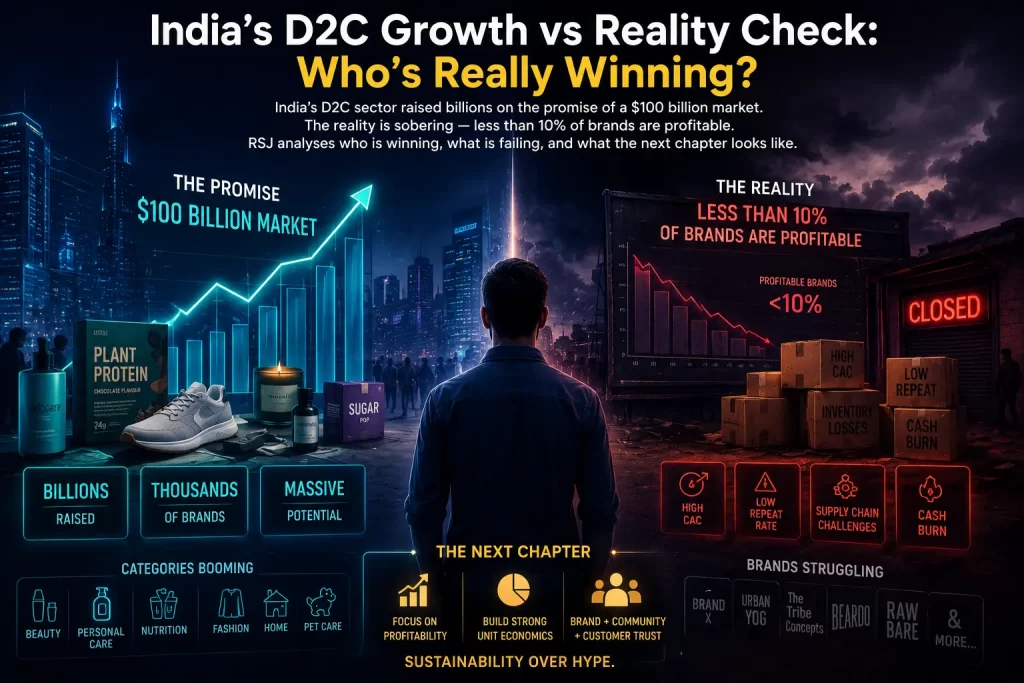

The Hype: A $100 Billion Opportunity?

Over the last five years, India’s Direct-to-Consumer (D2C) sector has been positioned as the future of retail. A 2022 report by Avendus estimated the market could cross $100 billion by 2025. That promise led to a flood of capital, with over 600+ D2C startups funded between 2019 and 2024, spanning personal care, food, fashion, home goods, and more.

Yet, as of mid-2025, cracks are beginning to show.

The Reality: Most D2C Brands Aren’t Profitable

While unicorns like boAt, Mamaearth, and Lenskart have scaled well, the broader D2C market is struggling with:

- Skyrocketing CACs (Customer Acquisition Costs)

- Heavy dependence on marketplaces (Amazon, Flipkart)

- Low brand loyalty

- Burn-heavy marketing without sustainable margins

In fact, a Bain & Co. 2024 study found that less than 10% of Indian D2C brands achieve sustainable EBITDA-positive operations after 3 years.

What’s Going Wrong?

1. CAC > LTV

The average CAC has grown 4X since 2020. With Meta ad costs rising and consumers tuning out paid campaigns, many brands are spending more to acquire a customer than they make from them.

2. Too Many Brands, Too Little Differentiation

Why should a consumer buy your plant-based shampoo over 99 others? This has led to a commoditization of categories like skincare, snacks, and home cleaning products.

3. Operational Nightmares

Logistics, warehousing, returns, and reverse shipping costs erode margins fast. Without back-end scale, D2C brands lose money on every order — especially in Tier 2–3 regions.

4. Lack of Brand Stickiness

Most D2C brands are discovery-driven — not habit-driven. If a customer forgets your brand next week, retention drops off a cliff.

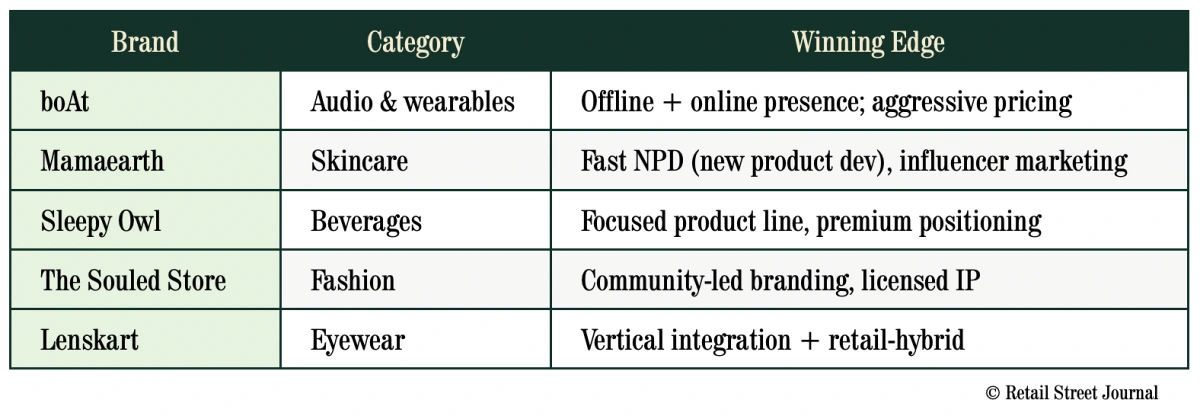

The Winners: Who’s Actually Scaling Right?

Here’s a list of Indian D2C success models worth noting:

The key pattern? Most of them evolved beyond “D2C-only” and now operate retail stores, kiosks, and omnichannel strategies.

Beyond Vanity Metrics: What Investors Now Demand

Gone are the days when “monthly order volume” or “Instagram followers” impressed investors. Today, they demand:

- Gross margin improvement

- Repeat customer % over 12 months

- Contribution margins post-fulfilment

- D2C + B2B hybrid models (like Mamaearth selling to Big Bazaar and DMart)

“We don’t fund D2C anymore unless it has a brand moat and offline expansion,” notes a top VC partner at Matrix Partners India.

The Future: D2C 2.0 Needs a Smarter Playbook

Smarter Distribution

- Expand into offline (retail shelves, popup stores)

- Partner with modern trade or Q-commerce players

Smarter Content

- Build brand communities (like Heads Up For Tails does with pet parents)

- Invest in owned media (YouTube, podcast, blog)

Smarter Tech

- Use AI for personalization (recommender engines, churn prediction)

- Use CRM + loyalty automation to boost retention

RSJ Insight: The Myth of Scale is Overrated

India’s consumer diversity demands deeper, not wider D2C strategies. Niche focus, strong value story, and smart omnichannel moves will define the winners in the next 3 years.

The Indian D2C dream isn’t dead.

It’s just waking up to reality.

Sources:

- Avendus Future of D2C Report 2022

- Bain & Co. Consumer India 2024 Report

- Matrix Partners Investment Notes (2024)

- RedSeer India Q4 2024 Consumer Trends

ABOUT THE AUTHOR

Rajalingam Rathinam

Founder of Retail Street Journal and NestOne Group. 30 years inside India’s largest retail businesses — Future Group, Landmark, Aditya Birla, Reliance, and Apple. Author of The Growth Matrix and From Clicks to Connections.

If you are a retail founder looking to build systems and scale without chaos — NestOne Group works with founders like you.

EXPLORE NESTONE GROUP →ALSO FROM RSJ

Need a laugh after all that strategy?

Read RSJ Comics — retail in 4 panels.